![]()

![]()

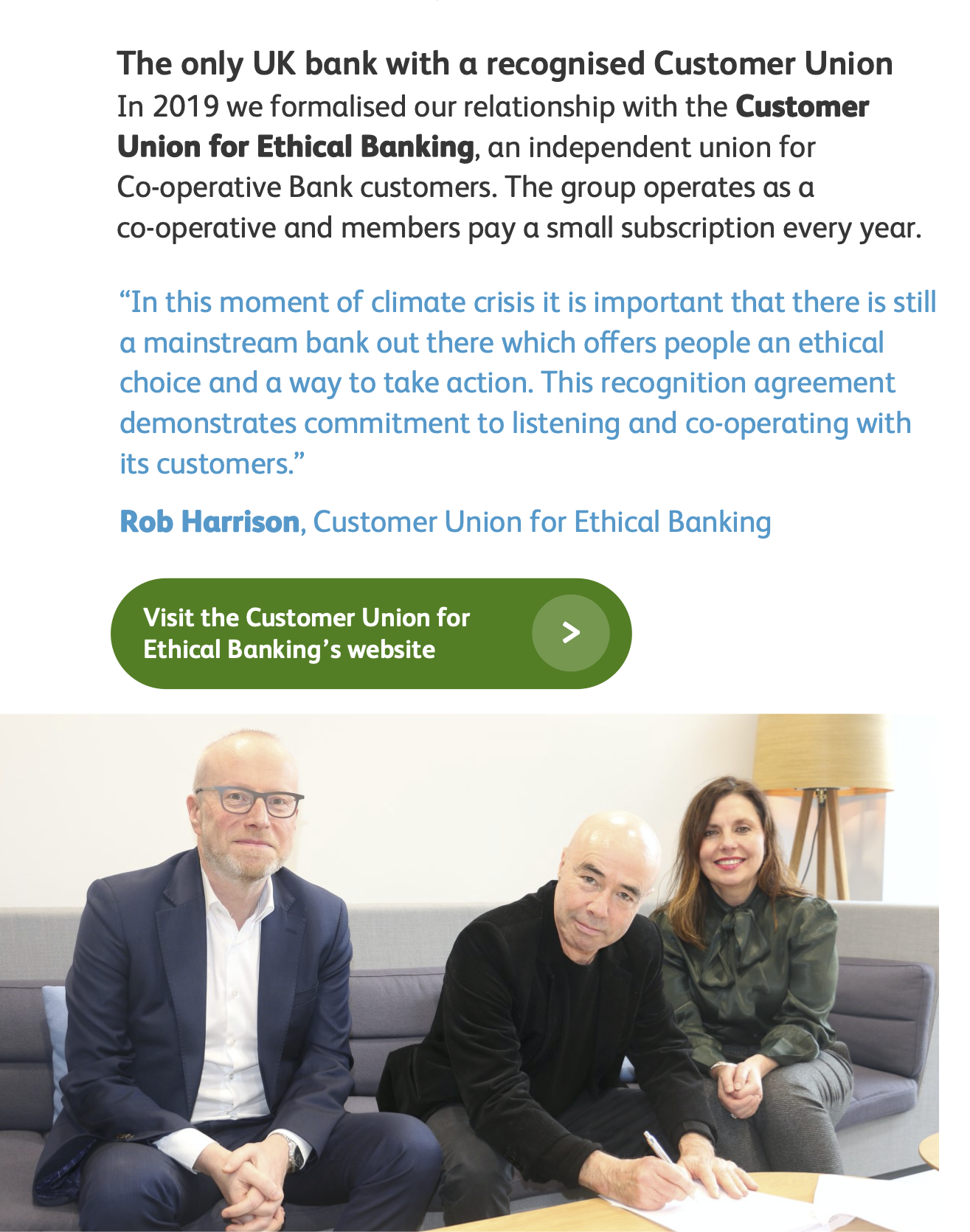

The Co-operative Bank’s Values and Ethics Report 2019: the Customer Union’s view

The Co-operative Bank’s Values and Ethics Report over 2019 was published on 18th May, and can be downloaded here. As a Customer Union dedicated to representing our members and ensuring the bank maintains its ethical commitments, we review this report carefully, raise questions with the bank, and share our observations with you.

Overall, the report is more extensive than the previous year’s (21 pages, after 2018’s fairly flimsy 12 pages), and it’s great to see the bank sticking to and extending its environmental commitments, working to address gender in management, and returning to a higher profile on human rights and climate change. We’re also pleased to see coverage of the bank’s recognition agreement with us at the Customer Union.

However we are disappointed that the bank, for the second year in a row, has chosen not to have the report externally verified, which we are concerned weakens the integrity of the bank’s Ethical Policy.

Here is our view of some notable aspects of the report. Do check the full report for more details, and get in touch with us if there are questions you would like us to raise with the bank.

No external audit for second year in a row despite commitment

Last year, for the first time since 1998, the Co-op Bank’s ethics reporting and Ethical Policy implementation was not subjected to external verification by a specialist sustainability auditor – an area in which the bank had previously led the way.

We called on the bank last year to address this, and the bank gave us a clear commitment in response (reported here) to “ensuring that next year’s report is subject to independent specialist third party audit.” This commitment was very welcome, and we are disappointed that the bank has not honoured it.

Although we understand that the Covid-19 crisis has played a role in the lack of external audit, our opinion is that these kinds of assurances should not be “nice to have” in fine weather only, but a cornerstone of ethical banking in the modern world.

We are calling on the Co-op Bank to make an early and firm public commitment to engage a named auditing team to perform a proper external audit, whatever the circumstances, of the 2021 V&E report. We will be launching a campaign early next year to make sure the bank acts on this. You can help by contacting the bank by email, Facebook or Twitter to let them know you are concerned.

Businesses declined for Ethical Policy reasons

The bank declined four businesses because of breaches of its customer-led Ethical Policy in 2019 – the same number as last year (but much lower than the 30+ businesses regularly turned away before the bank’s financial problems hit around 2013).

These were:

- Human rights: A consultancy serving the defence sector, which was considered in conflict with the bank’s policy on the manufacture or transfer of arms to oppressive regimes.

- Irresponsible marketing: A business that was making irresponsible marketing claims about the efficacy and safety of their product.

- Climate change: A consultancy business involved in the supply of equipment used in the extraction of oil, which was considered to conflict with the policy on fossil fuel extraction.

- Animal welfare: A business that manufactures equipment used as part of intensive farming practices.

The Co-op remains the only bank on the high street with an ethical policy based on customers’ concerns and the only bank to report on businesses declined in this way. One of our core aims is to defend the integrity of this policy, which is why the removal of independent scrutiny is such a concern for us and our members.

As before, accounts closed due to risk related issues, including concerns of money laundering and failure to meet customer due diligence requirements, dwarfs Ethical Policy declines. Such account closures have increased to 449 customer accounts from 410 in 2018 (up 9.5%). The bank has an Exit Forum to consider account closures since 2015, when it faced criticism from Save Our Bank and Amnesty for its closures of accounts for the Palestine Solidarity Campaign and other human rights groups.

The Hive and support for UK Co-operatives

The bank worked together with Co-operatives UK to create The Hive, a centre for advice and support of cooperative businesses. It reports that “since the start of the programme to the end of 2019, 941 groups have benefited from support”, an increase of 299 on the figure reported last year. It also provides a case study of Projekts MCR, the Manchester skate park under the Mancunian Way flyover which ran a community share offer with The Hive’s support.

The bank also notes that The Hive “is currently funded until the end of 2020” and that the bank is “working with Co-operatives UK to ensure that we continue to offer the best support we can to our co-operative customers.” We will ask the bank for an update on the future of The Hive at our next engagement meeting.

Managing environmental impact

At the Customer Union we often mention the fact that the Co-op Bank is the only high street bank with a clear policy against financing fossil fuel extraction. This is an important differentiator for the bank, but it’s not all they do on the environment front. This year’s report confirms that important aspects of its environmental management remain in place, including:

- Sourcing all electricity from renewables

- Reporting and reducing its operational greenhouse gas emissions (by 21% in 2019)

- Issuing only PVC-free credit and debit cards, and

- Supporting environmental projects overseas by offsetting its remaining carbon emissions plus an additional 10%.

The bank also has a new commitment to send zero waste to landfill by the end of 2020 (not long!), which we wish them luck with meeting. And it has received over 84,000 card readers from its customers for recycling. We have asked the bank what percentage of card readers issued this represents, and we’re awaiting a response on this.

“Proud signatories of the United Nations Principles for Responsible Banking”

The bank has announced in this year’s report that it has joined such ethical luminaries as the Industrial and Commercial Bank of China (ICBC, the world’s biggest bank and biggest banker of coal power), Barclays (Europe’s biggest funder of fossil fuels) and Citi (one the biggest banks in the US, which recently helped organise a massive share offer for Saudi Arabia’s state-owned oil company) in joining the Principles for Responsible Banking (PRBs).

If we sound underwhelmed, it’s because the PRBs were greeted with significant reservations by civil society groups when they were launched last year. Essentially, they allow all-comers to join, and allow banks to set their own targets. They may do some good, but the proof is in the pudding - we hope the Co-operative Bank sets itself some stretching targets to show that its signing of the PRBs makes a difference.

Addressing the gender pay gap?

As we’ve reported in the past, the Co-op Bank’s gender pay gap is one of the lowest in the industry, although there’s still work to do. The bank reports that it has already met and exceeded its target (set in 2016) to increase female representation in senior leadership to 40%.

The bank reports that for 2019 its “median gender pay gap was 22.62%, slightly lower than our 2018 figure of 23.31%.” This looks like a small but positive change. However, last year the bank reported on its mean gender pay gap, rather than the median figure. These are two different ways of expressing averages.

Checking the figures reported on the government website shows that according to the measure the bank didn’t report this year – the mean – women’s hourly wages at the bank are now 32.9% lower than men’s, compared to 29.9% in 2018. So on this measure the bank’s gender pay gap has got worse. The bank should not be cherry-picking data in this way, and we call on them to include both figures in future reporting. Perhaps an external auditor would have picked the bank up on this?

Verification statement from the bank’s Internal Audit team

In place of a statement from an external sustainability auditor, the bank’s 2019 report carries a “verification statement” from the bank’s Internal Audit function, which “concluded that the information in this report is accurate and not misleading.”

The bank set up a meeting between the Customer Union and the Internal Audit team so that we could ask questions about this Internal Audit process. This meeting left us reassured that the internal audit is indeed robust. However, this has never been a case of “either/or” – both internal auditing and external verification are needed to ensure strong controls over the bank’s ethics, and an external view is vital for maintaining trust.

The Internal Audit team, as an outcome from this meeting, told us: “we are very happy to answer any questions from members of the Customer Union for Ethical Banking, regarding the process we have undertaken to verify the data within the report.” Please let us know if you have questions for them.

@cuebcustomerunion.bsky.social

@cuebcustomerunion.bsky.social @saveourbank

@saveourbank