![]()

![]()

Following the merger of the Co-operative Bank and Coventry Building Society in 2025, the Customer Union began to reflect on what its role should be going forwards.

In our February 2026 newsletter, we circulated an online survey to all our supporters to seek a wide range of opinions. We received 805 responses and we provided a brief summary of these in our March newsletter too.

This longer article is for us to share more detail from the survey. We begin with two questions (Q4 and Q5) where respondents had free text fields to write what they wanted. In many ways the most interesting data is found here. We follow this with some graphs where respondents were asked to select from some multiple choice options.

Q4: What should the Co-op Bank do more of to lead on ethics?

1. Visibility, communication and public profile

The single most consistent theme across Q4 responses was a call for the Co-op Bank to be louder and more visible about its ethical credentials. A large number of respondents felt the bank was doing broadly the right things but failing to tell the world about it. Many urged the bank to promote its ethical policies more prominently in advertising, on social media, in mainstream press and even via cinema and TV campaigns.

Several pointed out that many potential customers are simply unaware the bank exists, let alone that it occupies a distinctive ethical position. The phrase ‘be proud’ appeared repeatedly, with respondents encouraging the bank to make its ethical stance front and centre in all marketing and branding, including on stationery and promotional materials. A few suggested targeted advertising at university fresher events or youth-focused platforms, reflecting concern that younger generations are not being reached.

2. Investment transparency and ethical screening

Many respondents called for greater transparency about where the bank invests and lends. They wanted clear, accessible information showing which sectors and organisations are supported or excluded, and why. Several drew comparisons with Triodos Bank, which was cited for its granular disclosure of lending decisions.

Respondents wanted to know not just what the bank avoids (arms, fossil fuels, oppressive regimes) but also what it actively invests in, suggesting the bank move toward a more explicitly ‘positive screening’ approach. A number of respondents also asked for externally audited ethical reporting, arguing that independent verification would give the policy greater credibility. Concerns about supply chain ethics and the ethical standards of the bank’s own technology and IT suppliers were also raised.

3. Palestine, arms trade and human rights

Many respondents urged the bank to take a stronger, more explicit stance against the arms trade, and to avoid any financial relationships with companies or states involved in human rights abuses. The situation in Palestine was the most frequently cited specific issue, with a substantial number of respondents expressing anger at the bank’s past de-banking of the Palestine Solidarity Campaign and similar organisations, and calling for this to be addressed and publicly acknowledged.

Others called for a blanket exclusion of investments connected to Israel. Some respondents extended this to calls for disinvestment from fossil fuels, oppressive regimes more broadly, and companies facilitating apartheid or genocide. A smaller number raised concern about animal welfare, urging exclusion of any investment in factory farming, animal testing or the meat industry.

4. Cooperative identity and employee practices

Another recurring thread was a desire to see the bank live its cooperative values internally as well as externally. This included calls for:

- A published pay ratio between the highest and lowest earners

- Recognition of trades unions

- Strong worker rights, fair sick pay and parental leave

- A commitment to keeping all services — including cleaning and security — in-house rather than outsourced

Some respondents also wanted the bank to formally demonstrate its cooperative identity by restoring its historical links to the Co-op Party and broader cooperative movement. Several pointed to the need for the bank to actively champion and fund cooperative development across the UK economy, including by offering preferential terms for cooperative and social enterprise clients.

5. Community investment and financial inclusion

A number of respondents wanted the bank to take a more active community role: funding local social housing, supporting food banks, creating community development loans, and ensuring that products and services are accessible to people who are digitally excluded, elderly, disabled, or on low incomes.

Specific suggestions included:

- Expanding multi-signatory account options for charities

- Offering free or subsidised banking to cooperatives and voluntary organisations

- Creating a network of community branch funds able to make local grants

Some called on the bank to support the development of community-managed lending agencies, particularly in areas of extreme poverty, as an alternative to exploitative payday loan providers.

6. Ethics in the digital age and AI

A smaller but notable cluster of responses raised concerns about the ethics of technology and data. These respondents asked the bank to be cautious about the use of AI and automation, to avoid outsourcing IT to large overseas cloud providers, and to maintain meaningful human contact in customer service. Several were concerned that the drive toward digitisation was itself an ethical issue, particularly for older customers who cannot or do not wish to bank online.

7. Dissenting and contrarian views

A minority of responses expressed scepticism or offered a different perspective. A few felt the bank’s ethical positioning was performative or too closely aligned with left-wing political causes, and argued that it should be more inclusive of right-leaning supporters of environmental and cooperative values. One respondent argued forcefully that self-proclaimed ‘leaders’ in ethics are often the least ethical in practice, advocating for humility and transparency over self-promotion. Another argued against gender identity policies, calling on the bank to align itself with recent court rulings on sex-based rights. These minority views, while not representative of the majority, reflect the breadth of opinion within the membership.

Q5: What else can we do together to be successful, ethical and co-operative?

1. The merger: concerns, hopes and oversight

While most respondents were broadly supportive of the merger, there were persistent concerns about what might be lost. Several asked for reassurance that the Co-op name would be retained, that the bank’s ethical policy would be applied in full across the merged entity, and that Coventry’s own business clients and practices would be subject to the same ethical screening.

A number of respondents reported feeling uncertain or anxious about what the merger meant for them as customers, and requested clearer, more frequent communication from both institutions. Some wanted the Customer Union to take an active watchdog role, monitoring compliance with ethical commitments throughout the merger process and beyond. A few were also worried about the structural governance of the merged entity, calling for one-member-one-vote democracy and transparent conflict-of-interest policies.

2. Branch access and physical banking

Access to physical banking was among the most emotionally charged topics. Many respondents expressed frustration or sadness at the loss of local branches, with some noting that their nearest branch was now dozens of miles away. Several pointed to Nationwide as a positive model of maintaining high street presence. Respondents called for the merged bank to explore shared branches, mobile banking vans for rural areas, and expanded participation in banking hub schemes. The need to protect non-digital customers — including older people, disabled people, and those without smartphones — was raised repeatedly. Some respondents linked physical access directly to the bank’s ethical mission, arguing that a genuinely ethical bank cannot exclude people who lack digital access.

3. Customer service and digital functionality

A significant number of respondents raised practical concerns about the quality of day-to-day banking. Long telephone waiting times were a recurring complaint, with several respondents contrasting this unfavourably with other banks. The functionality of the mobile app was also criticised, with respondents noting the absence of features available elsewhere — such as international transfers, better fraud controls, and improved two-factor authentication options including landline and email alternatives. A few respondents went further, suggesting the bank was at risk of losing customers to more digitally capable competitors, and argued that being ethical should not mean accepting poor service!

4. Cooperative governance and member democracy

Several respondents called for the merged entity to operate with genuine cooperative governance — not simply in name but in practice. This included calls for:

- Customers to be invited to hold shares and participate in annual votes

- The Customer Union to have formal representation on the bank’s board

- Decisions on controversial ethical matters to be put to members rather than determined by management alone

Some expressed concern that the Coventry Building Society rarely meaningfully consulted its members, and hoped the merger would bring a more participatory culture. A few respondents also asked for the bank to commit to a published salary ratio between its highest and lowest paid employees, and to ensure this commitment was binding rather than aspirational.

5. Marketing, awareness and younger customers

Across many responses ran a concern that the bank’s ethical identity was invisible to most people, particularly younger generations. Respondents called for more imaginative and targeted marketing, including a presence at university events, youth festivals and community forums. Some suggested the bank should more explicitly name and shame the unethical practices of mainstream banks — pointing out, for instance, that moving your money to an ethical bank may have a greater climate impact than many individual lifestyle changes. One respondent offered to assist pro bono as a content strategist. Several called for the bank to collaborate with other ethical financial institutions and campaigns. The bank’s historical connection to the Co-op supermarket was seen by some as an underused asset for reaching a wider public.

6. Ethical investment products for customers

A number of respondents noted a gap in the market for genuinely ethical savings and investment products. They wanted the bank to offer ISAs and pension products where deposits are ring-fenced for ethical lending or green projects, and where customers can trust that their money is not being invested in fossil fuels, arms or exploitative businesses.

The difficulty of finding ethical pension providers was raised by several respondents as a personal concern, particularly among those on lower incomes who cannot afford to lose returns by choosing niche ethical funds. There was clear demand for pre-packaged, accessible ethical investment options that do not require specialist financial knowledge.

7. Tone of engagement and appreciation

Many respondents took the opportunity to express warm appreciation for the Customer Union and the bank’s direction of travel. Phrases such as ‘keep up the good work’, ‘you are doing great’ and ‘I am proud to be a member’ appeared throughout. Several respondents were positive about the act of being surveyed at all, noting that being asked for their views was itself a marker of genuine cooperative values.

A smaller number were more cautious, urging the bank to ‘be brave’, ‘stick to your principles’ and not be swayed by short-term commercial pressures or vocal minorities. A few dissenting voices expressed concern that the bank had already compromised its ethics and called for more rigorous accountability.

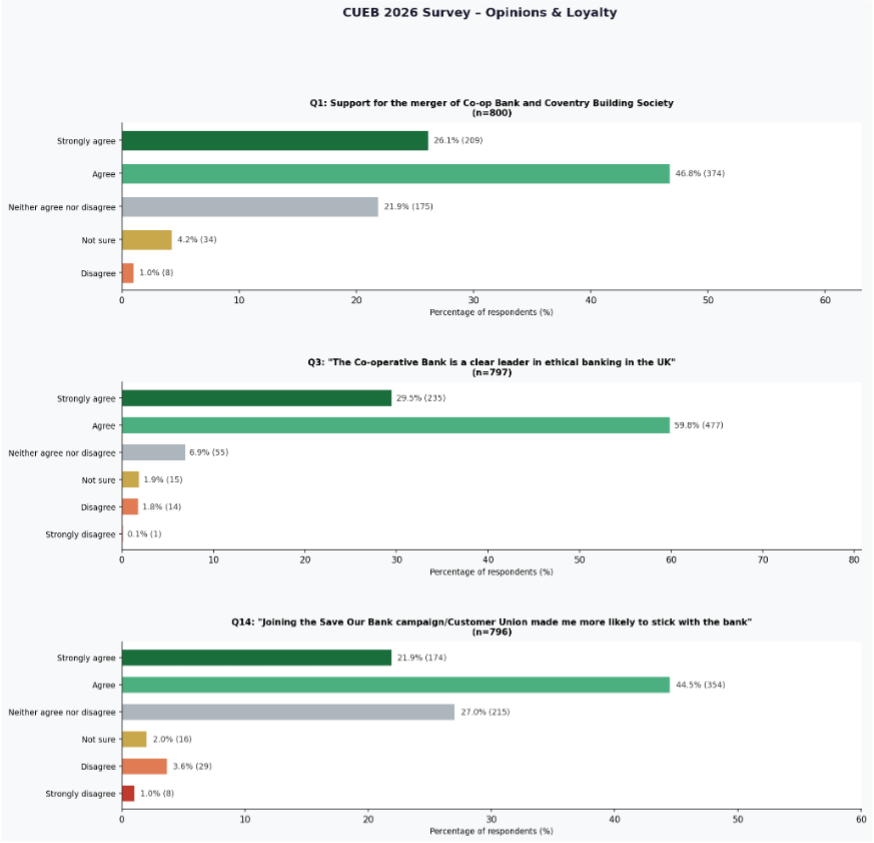

Quantitative questions results

- Strong mandate for the merger. 72% support it (agree or strongly agree), with only 1% opposed. The 22% “neither” likely reflects genuine uncertainty about what the merger means in practice rather than opposition.

- Ethical reputation is a core asset. 89% regard the bank as a clear leader in ethical banking — an unusually high score.

- Ethics and the co-op identity are the main retention drivers. 94% cite one or both as why they stay. This suggests the ethical brand is genuinely load-bearing, not just nice-to-have.

- Customer Union membership builds loyalty. Two-thirds say joining made them more likely to stick with the bank — a meaningful finding for member engagement strategy.

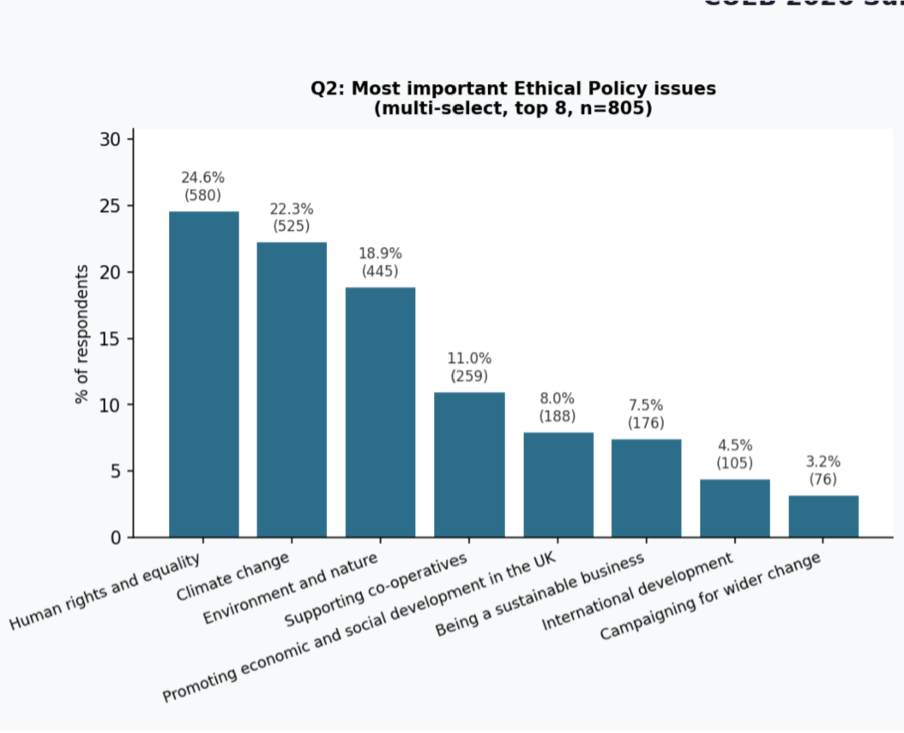

Ethical Policy Questions

Human rights & equality, climate change, and environment top the list of priorities, well ahead of other issues.

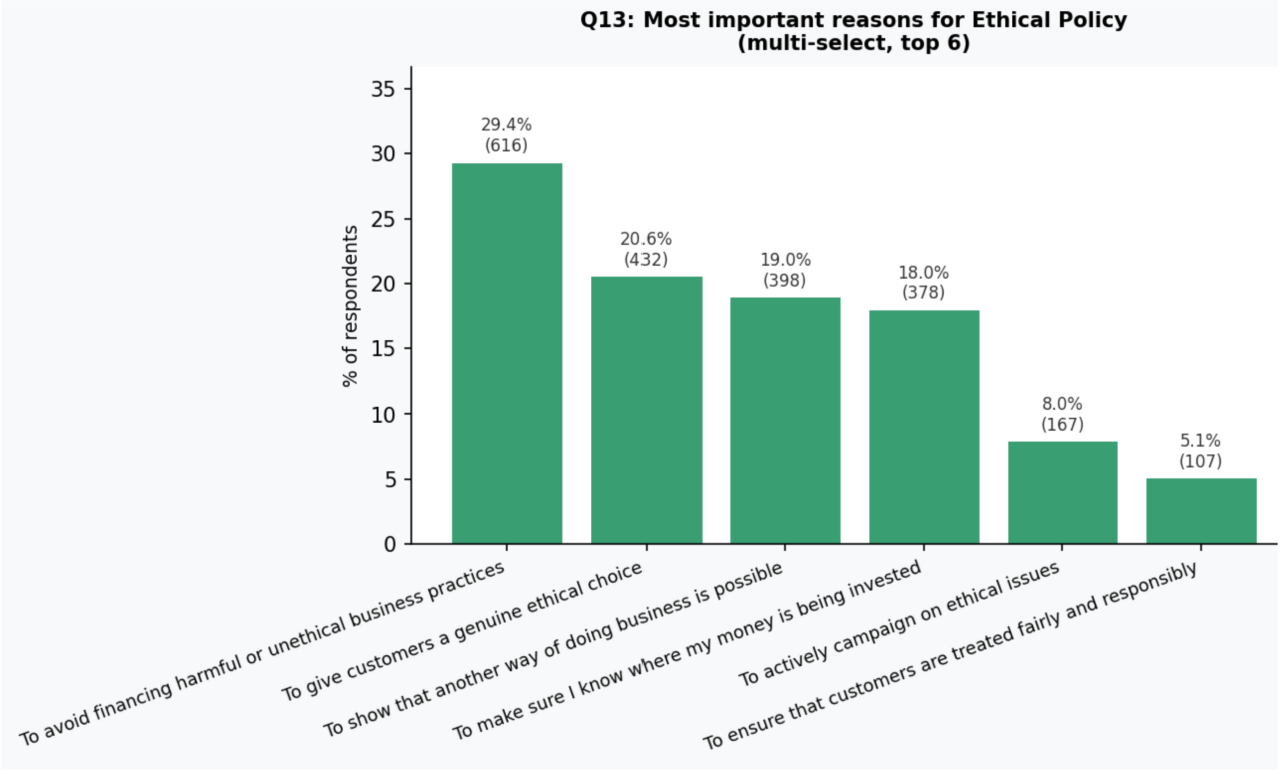

Avoiding harmful financing (76%) dominates as the reason people want an ethical policy to exist.

The survey also contained questions about demographics, CUEB gatherings, and how people liked to communicate with us. We have not shared information from these internal questions here.

This survey analysis used Claude AI to help draft the text. It was subsequently edited by a human. CUEB are currently developing a more formal ethical policy around the use of AI tools.

July 2026

@cuebcustomerunion.bsky.social

@cuebcustomerunion.bsky.social @saveourbank

@saveourbank